Navigating the world of insurance can be complex, especially when it comes to advanced strategies like split-dollar plans. These plans offer unique benefits for both the organization and the executive, making them a valuable tool in financial planning and organizational strategy. In this blog, we’ll delve into what split-dollar plans are, how they work and their advantages.

What is a Split-Dollar Plan?

A split-dollar plan is a method of purchasing life insurance in which an organization and an executive share the costs and benefits of the policy. These plans are typically used as part of executive compensation packages to provide key executives with life insurance coverage and retirement benefits, while allowing the organization to recover its costs.

There are two main types of split-dollar plans: loan regime and economic benefit regime. In a loan regime split-dollar plan, the executive owns the policy and assigns a portion of the death benefit to the organization as collateral for the premiums paid. Conversely, in an economic benefit regime split-dollar plan, the organization owns the policy and endorses a portion of the death benefit to the executive during employment. For the remainder of this article, we take a deeper look at loan regime split-dollar, commonly used by organizations as an effective retention and recruitment tool.

In a typical loan regime split-dollar arrangement, the organization and executive agree on how the premium payments, cash values and death benefits will be shared. The plan can be structured in various ways to meet the specific needs of both parties, including as a single-policy structure or a dual policy structure. We explore these two popular structures below, including the benefits each structure offers.

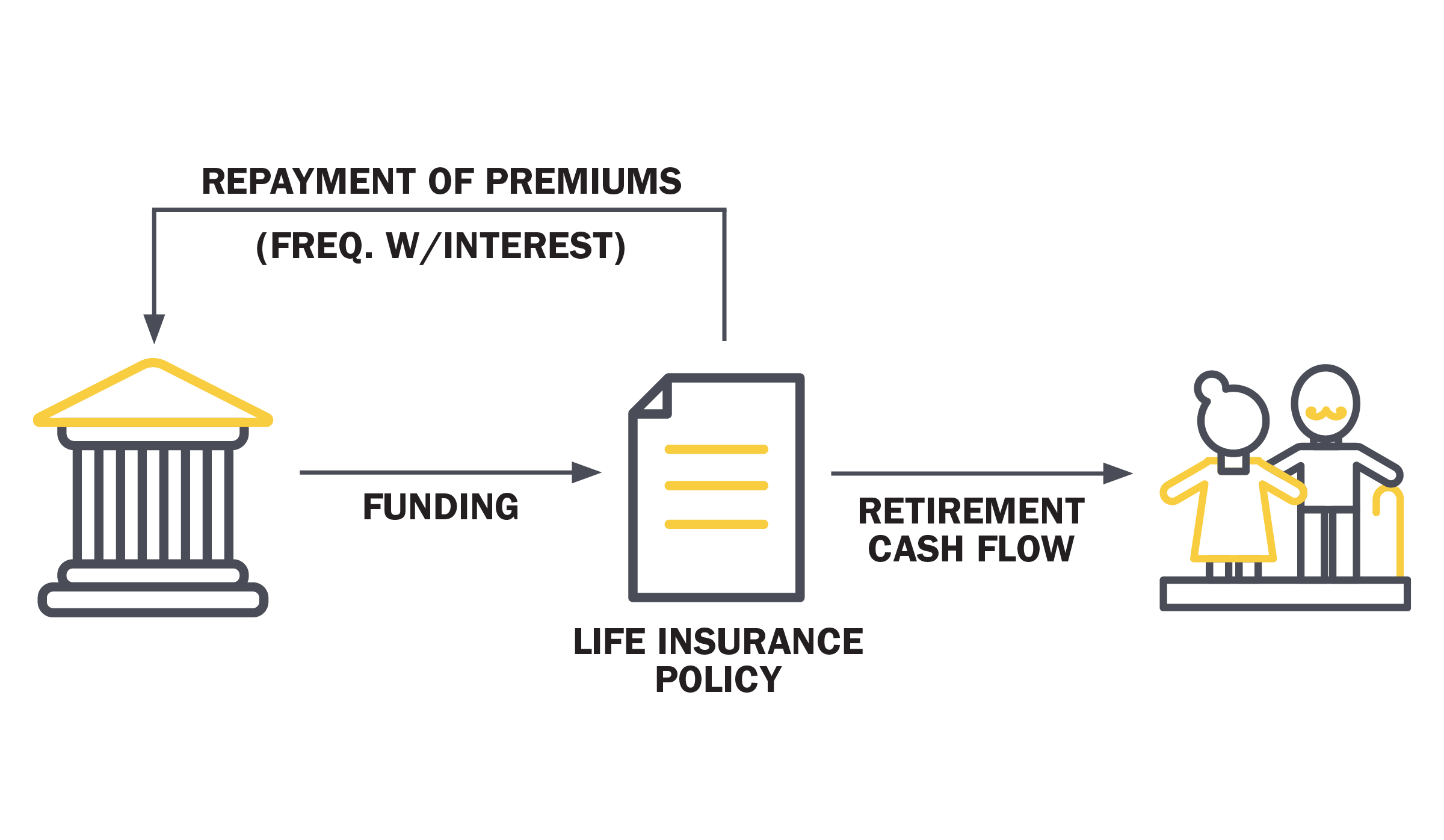

Single Policy Structure

In a single policy structure, only one life insurance policy is issued and is designed to meet the objectives of both the organization and the executive. This means the policy’s premiums, cash values and death benefits are shared according to the terms agreed upon in the split-dollar arrangement. The premiums the organization pays to the policy are considered loans to the executive for tax purposes. In return, the organization must be repaid its premiums, often with interest, from the death benefit of the policies. The remaining death benefit is designated for the executive’s beneficiaries, or shared between the beneficiaries and the organization.

How It Works:

- Premium Payments: The organization pays the premiums recouping these funds through the policy’s cash value or death benefit.

- Policy Ownership: The policy is owned by the executive and collaterally assigned to the organization, with clear terms outlining each party’s rights.

- Policy Benefits: The executive accesses the cash value of the policy during retirement, or as otherwise permitted by the split-dollar agreement.

- Benefit Distribution: Upon the insured’s death, the organization recovers at a minimum the premiums paid, often with interest, and the remaining benefit goes to the executive’s beneficiaries or is shared among the organization and beneficiaries.

Benefits:

- Simplicity: With one policy, there’s less administrative burden, making it easier to manage and for the parties to understand the split dollar agreement. Administration becomes more burdensome during retirement when the parties must agree upon the executive’s retirement access so plan compliance is not jeopardized.

- Upside Efficiency: If the policy outperforms expectations, the executive can usually access the additional value above what is necessary to cover the obligation to the organization. This is due primarily to the increased funding required to implement a single policy design.

Single Policy Structure

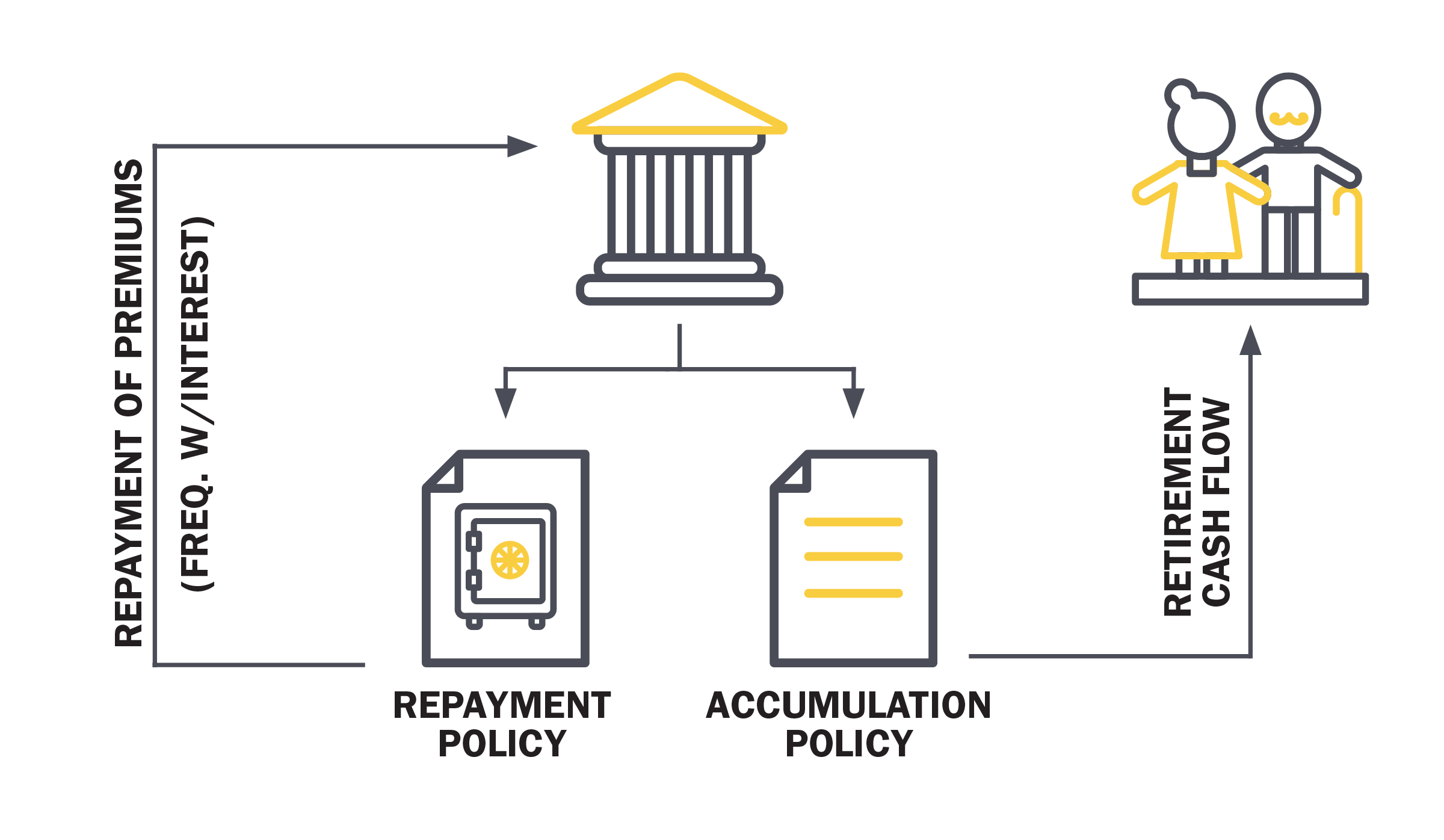

Dual Policy Structure

In a dual policy structure, two separate life insurance policies are issued: designed to achieve separate objectives. One policy is designed to accumulate death benefits specifically to meet the obligation to the organization, while the other policy is designed to accumulate cash value, and provide retirement benefits to the executive. Each policy serves different purposes but is part of a cohesive split-dollar agreement.

How It Works:

- Premium Payments: The organization pays the premiums recouping these funds through the policies cash value or death benefit.

- Policy Ownership: The policies are owned by the executive and collaterally assigned to the organization, with clear terms outlining each party’s rights to each policy.

- Policy Benefits: The executive accesses the cash value of the policy designed to provide retirement benefits, but has no access to the policy designed for the organization’s obligation.

- Benefit Distribution: Upon the insured’s death, the organization’s policy covers the premiums paid, often with interest. The executive’s policy provides a residual death benefit to their beneficiaries.

Benefits:

- Flexibility: This structure allows for more tailored solutions, with each policy designed to meet specific needs of the organization and executive.

- Control: The parties have specific rights over their respective policies, making it easier to manage the inherent competing objectives of the plan. For example, the organization’s policy is kept separate from the executive’s retirement benefit activity, ensuring the obligation to the organization is protected. The organization and executive typically also retain the right to direct investment allocations in only their policy, easing potential for disagreements post retirement.

- Diversification: Dual policy structures allow for more diversification between insurance carriers and products to meet the needs of each party.

- Enhanced Benefits: Dual policy structures are often less capital intensive, or can provide enhanced benefits, than single-policy structures, due to the efficiencies of separately designed policies.

Dual Policy Structure

Both single and dual policy structures offer unique advantages, depending on the needs of the organization and executive. Single policy structures are simpler to understand, often making them ideal for smaller organizations or straightforward agreements. Dual policy structures, on the other hand, provide greater flexibility and control, making them suitable for more complex financial arrangements. When considering which structure to choose, it’s essential to consult with a financial advisor to determine the best fit for your specific circumstances and goals.

Considerations and Risks

While split-dollar plans can be advantageous, they are also complex and come with certain risks:

- Complexity: Setting up and maintaining a split-dollar plan requires careful planning, legal documentation and compliance monitoring. It’s crucial to work with experienced advisors to ensure compliance with tax laws and regulations.

- Tax Implications: Depending on the plan’s structure, there could be unintended tax consequences. This makes it crucial for organizations and executives to partner with experienced firms with demonstrated capabilities in plan design and implementation.

- Termination: If the executive leaves the company or the plan is terminated, there must be clear provisions for how the policy’s cash value and death benefit will be handled.

Unlock the Benefits of Split-Dollar Plans

Split-dollar plans are a powerful tool in financial planning, offering unique benefits to both organizations and executives. By understanding the basics of how these plans work and their potential advantages, you can determine if a split-dollar arrangement might be right for your needs.

Call us today at 972-318-1110 to schedule a consultation and take the first step toward a more secure financial future. Your peace of mind is worth the call.